Health Insurance

Health Insurance

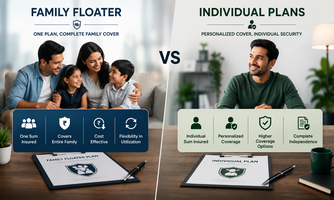

7 Things to Check Before Buying Health Insurance

Most health insurance comparisons stop at premium and sum insured. These seven factors often determine whether coverage holds up when it matters most.

Discuss With Advisor